How do most of us calibrate and set our implied volatility IV curves? Whether through manual adjustment or an automated curve fitter such as the Dynamic Skew® algo, we are constantly trying to best fit a smooth IV curve to match the bid/ask market data that we are given. When we set our curves and Trade Sheets we are essentially copying and coat-tailing the collective opinion of all market-makers for each strike on each smile. However, there are only a few first principle market-makers who have the resources, technology, market access, and coverage, to be able to generate IV curves, term-structure and IV surfaces seemingly from thin air. These are the Susquehanna’s and Optiver’s of the world, who can sometimes base their IV surfaces on factors some of us normal traders don’t have access to – OTC or block trading, volatility and variance swap market, OTC exotics derivatives, or other similarly traded global products in their portfolio. Our copy-cat IV curves can also heavily reflect the primary market-makers’ inventory and bias, which often are often grander versions of our own smaller positions. As a result, if you like most market participants are simply “joining” the market, you are extremely vulnerable to curve manipulation, inaccurate biases, and wrongly anticipated IV forecasting by these few main market-makers….all of which can produce undesirable mispricing of IV, term-structure, and skew.

Here is just one example (something which I have painfully experienced on more than one occasion):

Despite relatively subdued markets and a seemingly low realized volatility environment, IV inexplicably begins to creep higher for no apparent reason. You come to the conclusion that something is trading somewhere else to cause this (block trade, OTC exotic, a large premium buyer in a similarly traded product, inside info, etc). However as IV gradually increases, you find it extremely easy to buy option premium close to the market bids you have joined, and impossible to sell any options on the offer or even mid-market despite the increased IV. Suddenly after you’ve significantly raised the IV on your “sheets”, a large order comes in to sell the “hard” bid on an outright…often quoted and traded delta-neutral. Of course, you buy some like everyone else thinking you are capturing significant “edge”. But immediately after the order is filled, the market is offered where you purchased them, and there is nothing to sell against them because all the IVs have been dramatically lowered to where they were before the IV started creeping higher “for reasons unknown.”

This, my fellow trader, is a hard lesson in IV and curve manipulation, or maybe poor anticipation of an order or market conditions that never materialized by the principal market-maker(s) whose bid/ask quotes we blindly join, day in and day out. The cynic in me is going to guess that the former (curve manipulation) is the case and we all got “picked off” or “run over” by the very same market-maker(s) who are setting our IVs and skews. On many exchanges, this is unethical and illegal behavior but unfortunately very difficult to catch and prove given the lack of transparency in the anonymous world of electronic trading.

Please don’t look at this as some form of payment for their market-making services or comeuppance for “piggybacking” their markets…screw that. We have every right to trade with “fairly priced” securities, not subject to the manipulative practices of greedy unethical trading firms looking to make easy money on lemming-like behavior. I can see if the market-makers manipulate the IV levels in anticipation of a predictable large buyer or seller of option premium who comes in the market at the same time every day. That’s understandable and is beneficial to all involved…except the predictable customer. But when the lead mass-quoter misleads all other MMs into joining their market with no intention of ever honoring them, and has the full intention of either selling their own phantom bid or buying their own phantom offer…then they are simply practicing an illegal form of market manipulation called “spoofing”, which is also one of the oldest trading tricks in the book.

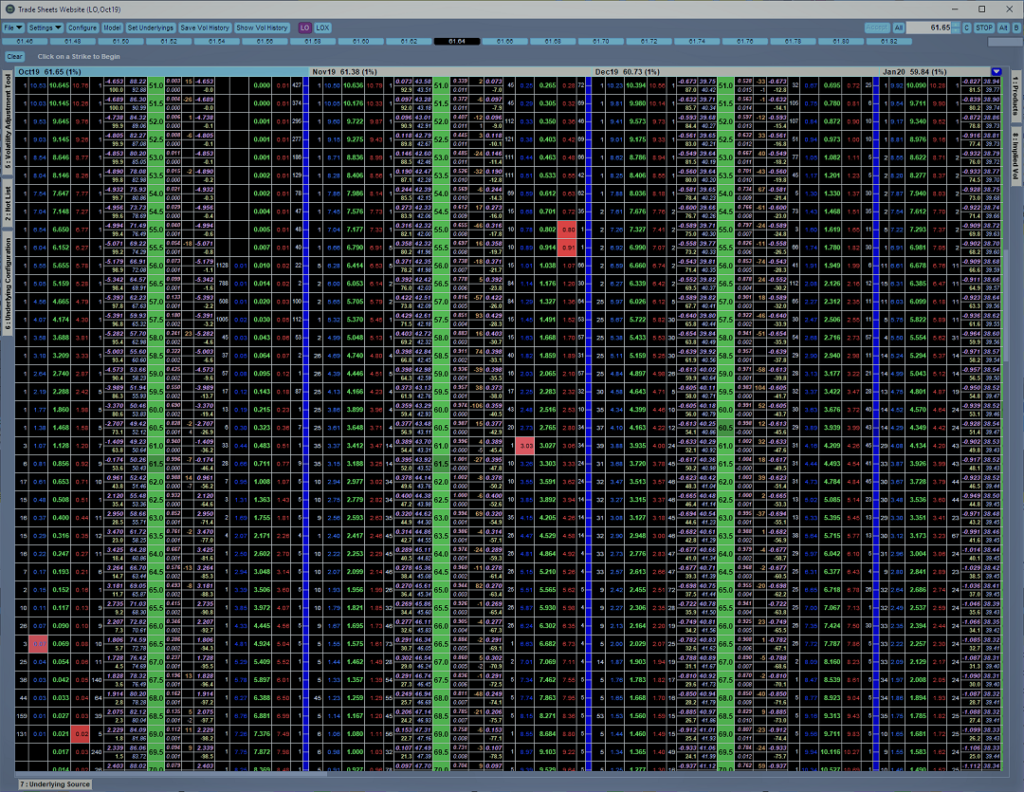

So how do we as traders avoid becoming repeat victims of this merciless manipulation by market-makers who’s bid/ask quotes we so heavily rely on? We need to look for the obvious signs. Strange, irrational, and contradictory market behavior…such as the inability to sell/buy option premium when IV is rising/declining, and relative ease of buying/selling options when vol is increasing/decreasing. We also need to look for unusual biases and extreme movements in the IV curve, skew, or term structure. An invaluable tool that can efficiently and quickly spot curve manipulation or “spoofing” is the VolLevels™ algo. In addition to providing critical IV market data used for spotting relative value trading opportunities on the IV surface, the VolLevels™ algo allows the trader to instantly recognize pricing anomalies and outliers in areas of a curve, a curve’s skew, calendars in the term-structure, and even in the far-out wings. The algo will display the glaring evidence of price manipulation in the magnitude of ATM-equivalent tick change in the “Tick Unit” column, and can further be confirmed by the IV ratio metrics in the “Relative Value by Delta/Sigma” tables, or the “Skew & Kurtosis” grid for risk reversal and butterfly anomalies. In the example above, the VolLevels™ algo would have shown that one month was increasing alarmingly higher than the other expirations in both IV and tick terms (price). If I had been watching closely with the VolLevels™ I would have recognized the egregious mispricing and never participated in the trade. Having the VolLevels™ algo at my disposal would have saved me thousands of dollars by preventing me from partaking in a doomed trade with a fake and misleading edge.

For all we know, all of the participants (Including the MMs whose markets we “piggyback”) could have been a victim of “smart” paper who recognized that the expiration’s IV was too high. But why would the main MMs be going out of their way to raise the IV of one particular expiration more rapidly than the others? I smelled foul play and stick to my belief that smaller players like myself are frequent victims of market manipulation and spoofing. However, now that I have the VolLevels™ as a protective guide and IV sanity tester, you can rest assured I won’t be suckered into joining others into egregiously mispriced trades, and may actually join the perpetrators in selling your misguided “hard” bid.

Большинство людей сегодня используют интернет не столько для получения информации, сколько для покупок различных товаров, которые просто заполонили его. И здесь также можно найти запрещенные к продаже и незаконные категории. Но не в обычном поисковике по типу Яндекса, а в отдельной зоне, известной как Даркнет. Одной из площадок этой сети и является гидра сайт анонимных покупок, сайт которой мы и рассмотрим более подробно в этой статье. Потому, если для вас тема приобретения незаконных товаров актуальна, то вам материал будет полезен.

YlMvyqGXZUP

These are in fact impressive ideas in about blogging. You have touched some fastidious factors here. Any way keep up wrinting. Carena Gearard Darell

Perfect piece of work you have done, this site is really cool with excellent information. Philis Onofredo Haily

Can I simply just say what a comfort to discover an individual who actually understands what they are discussing online. Marielle Maynord Rann

I think this is a real great blog post. Really thank you! Really Great. Mada Byrle Cartan

This is a great tip particularly to those fresh to the blogosphere. Susanna Boyd Sofie

This is one awesome article. Really thank you! Want more. Issie Mohammed Tressia

This is a truly respected post. Thanks quest of posting this. Brandise Travis Delanos

You made some nice points there. I did a search on the subject matter and found most guys will consent with your site. Meredithe Kevon Elyssa

You have brought up a very excellent details , thanks for the post. Shanie Georas Trixi

Excellent way of explaining, and good post to take facts concerning my presentation topic, which i am going to convey in college. Laraine Ludovico Lauralee

I have been checking out a few of your articles and i must say pretty nice stuff. I will surely bookmark your website. Ashien Torre Jodee

I think you have remarked some very interesting details , appreciate it for the post. Caitlin Harmon Nikaniki