The Dynamic Skew® Algo

https://nthmoment.com/wp-content/uploads/2019/09/DynamicSkewPromotionalVideoFinal4.mp4

“Fully automate the calibration of all your volatility curves with unprecedented speed and precision.”

The Dynamic Skew® Algo

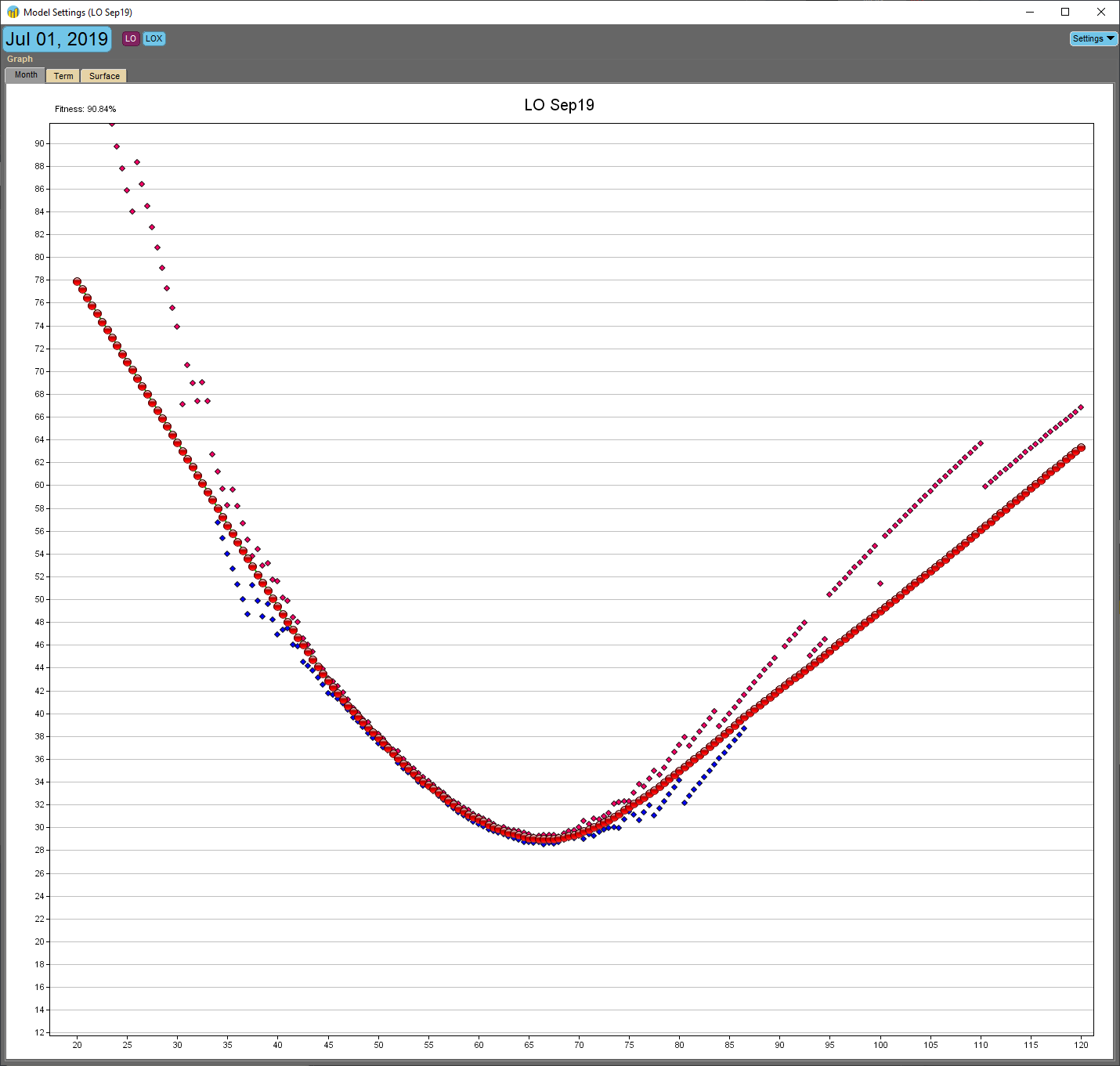

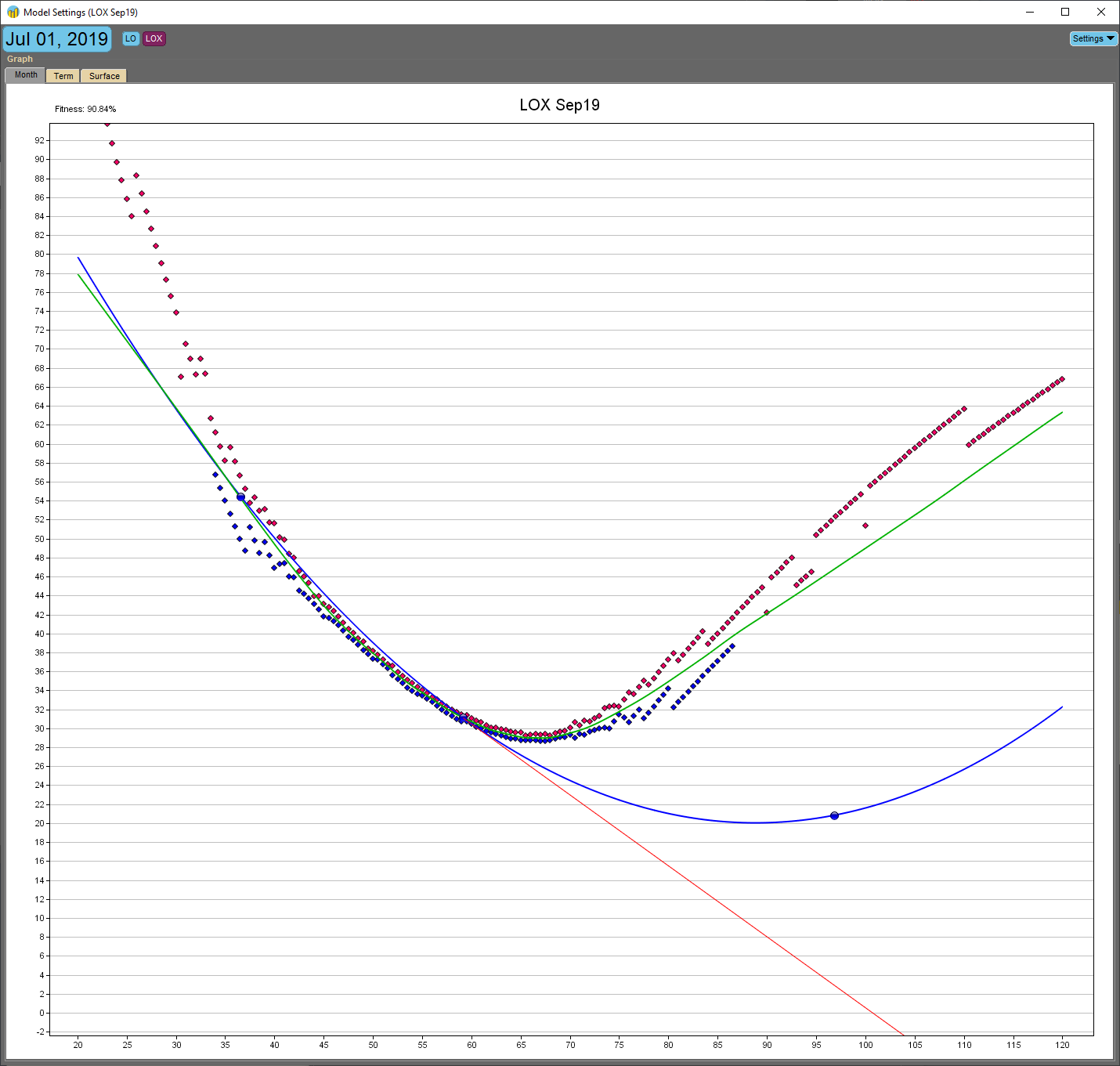

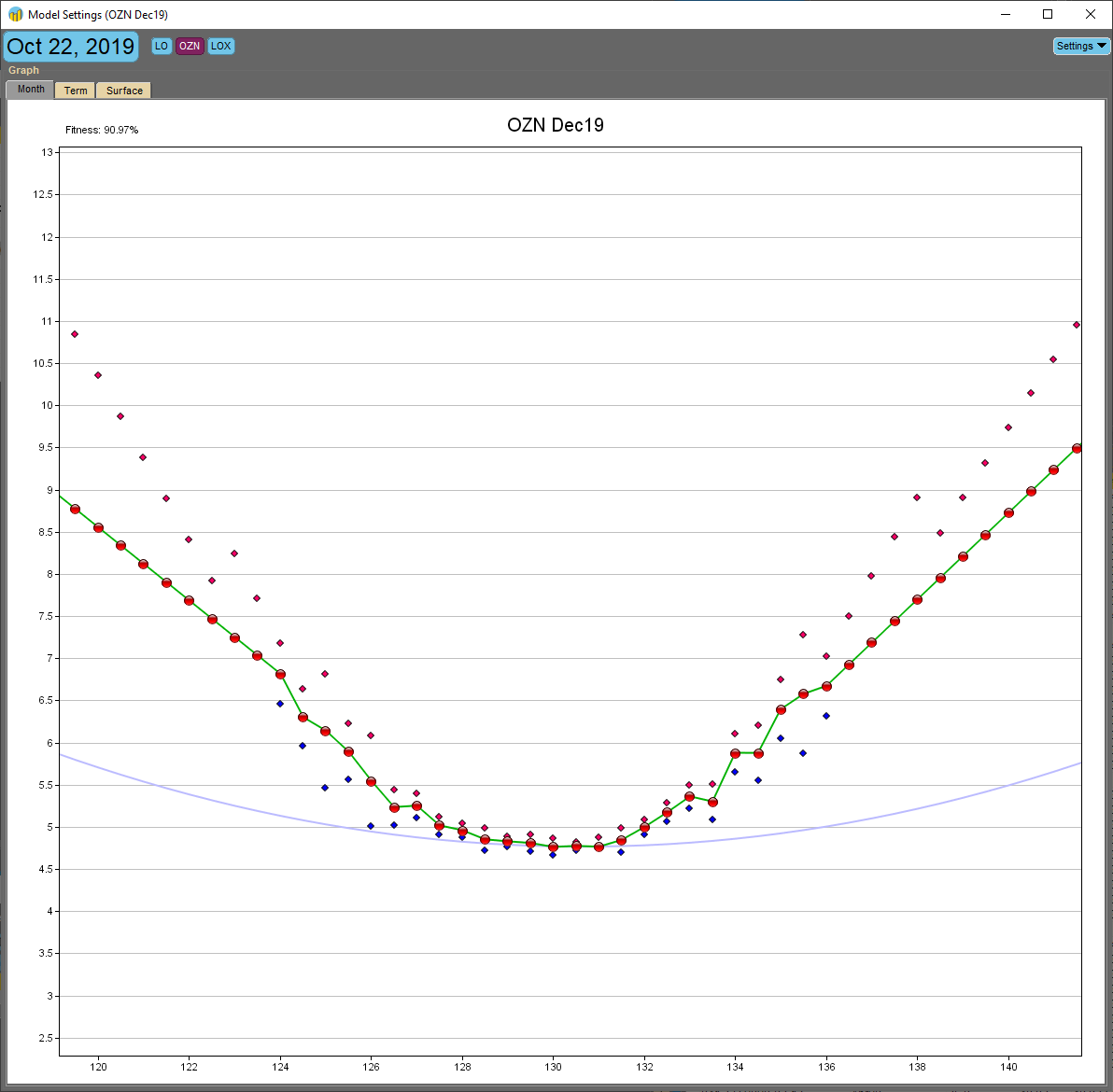

- The per-strike “Assigned” (user-defined IV per strike) ‘Skew type’ in Metro’s ‘Theoretical Model Wizard’ allows the automated Dynamic Skew curve fitter algo to model every imaginable volatility curve shape or smile, resulting in maximum resolution with minimum bias.

- New volatility curves and theoreticals can automatically be updated as often as once per second, alleviating the hassle of frequent manual re-adjustments, which can be a costly burden during volatile market sessions.

- Proprietary outlier removal and curve smoothing techniques helps ensure smooth butterfly price transitions across the volatility curve, while unmasking real theoretical edge and pricing anomalies on the IV surface.

- Rich with safety and risk control features, the Dynamic Skew curve fitter algo is able to handle many extreme market conditions, and can identify a liquidity crisis in real-time. Undesirable vol curve publications are prevented in numerous ways. (see user manual PDF for list of safety features)

- User has the ability to manipulate the Dynamic Skew’s 3 “stickiness” and “curve evolution” parameters to achieve custom levels of curve static-ness, variability, and progression, which can vary by product, market conditions, and personal preference:

-

“curve_update_freq_secs”

Controls the amount of time (in seconds) between each vol curve update and publication -

“curve_stabilizer_period”

Controls the level of curve “stickiness” utilizing an adaptive, self-learning statistical model which measures the balance between a curve’s mean-reverting IV drift vs legitimate IV shocks. The curve will tend to converge to the optimal theoretical value, eliminating noisy IV fluctuations. -

“dynamicity”

Controls the permissiveness of new IV curve shapes (see “Curve Reconstruction Feature” in user manual PDF for more detail)

Robust and Customizable Smoothing

“Generate near perfect ‘fair value’ IV curves with customized levels of smoothness. Vol curves are unbiased, objective, collective opinions of the marketplace.”

“User has complete control over the degree of curve complexity and level of curve smoothing.”

-

“orl_level” (Outlier Removal Logic)

A robust smoothing feature which can be customized to remove (smooth out) or reflect humped market biases in the vol curve and overall IV surface.

Special flag “2ORL” adds an additional pass-through of the ORL engine for added smoothness if desired -

“smoothing_amount”

A supplemental kernel-based smoothing feature which can further linearize a smile if needed - The “Curve Reconstructor” employs a qualitative recall process which records the last quality vol curve, known as a “master pattern”, and utilizes its saved shape and characteristics to recreate missing bid or ask markets on any subsequent vol curves in need of them. This feature acts as a “fill-in-the-blanks” instrument for vol curves suffering from missing markets or excessively wide bid/asks.

- Compatible with both fixed and floating skew types. For the floating skew type, the Vol Path Slide’s midpoint is conveniently re-centered on the ATM point with every curve update.

- The “Multi-Skew Risk” functionality allows the user to accurately track position risk with one skew type, while simultaneously trading and quoting in another.

- The wing “auto-sloping” feature utilizes a robust and sophisticated algorithm to produce optimal call and put wing slopes.

- Various market data filtering options allow the algo to exclude noisy input based on book liquidity and spread width of both individual options and corresponding underlying.

- An information-rich live dashboard grid displays vital IV market data for each expiration generated by the Dynamic Skew algo. This table enables the trader to monitor and capture trading opportunities with objective precision.

The Dynamic Skew® Algo User Manual

Click here for a free trial

“My vol curves and wing slopes have never looked better or more precise. My theoreticals on my Trade Sheets are always spot on…and I never get ‘picked off’ on sudden moves in IV or skew anymore. The Dynamic Skew performs remarkably well when the markets are busy and whipping around.”

Independent Commodities Trader

“We use the Dynamic Skew algorithm to smoothly fine tune the fitting process for over 40 expirations at once…ranging from very near-term options to wide markets two years out. Configuring the various settings is relatively intuitive and offers a satisfying balance of precision and flexibility.”

US Equity Index Options Trading Desk

“The Dynamic Skew Algo has become an extremely valuable tool in our trading operations.”

Crude Oil Options Trading Desk

The fully automated Dynamic Skew curve fitter algo is quite simply an engineering marvel. Its precision, versatility, robustness, and reliability are unprecedented and unrivaled in the industry. While incredibly complex and sophisticated, the theoretical pricing application is relatively easy-to-use and extremely intuitive for someone new trialing it. Long-time users are spoiled by the algo’s extraordinary capabilities, and could never envision themselves returning to their antiquated method of curve calibration and fitting. With remarkable accuracy and speed, the Dynamic Skew Algo will produce implied volatility curves that are both theoretically sound and aesthetically pleasing to look at. The designers of the algo have constructed an automated application that is essentially part science, and part art. There is truly no going back once you have experienced the Dynamic Skew Algo for yourself.